Prysmian Starts the Year with Organic Growth, Margin Expansion and Strong Free Cash Flow

- Revenues rise (+5.0% organic growth), and profitability is enhanced (14.2% margin vs. 13.1%, Q1’25)

- Transmission sets best-in-class margins (20.1% vs. 16.9%, Q1’25)

- Organic growth in Power Grid accelerates (+16.2%)

- Excellent quarter for Industrial & Construction as Revenues increase (+5.8% organic growth), thanks to North America (+10% organic growth), driven by data centers

- Digital Solutions continues positive momentum as fiber demand for data centers boosts organic growth (+9.0%). Channell drives margin acceleration to 20.6% (+7.4 p.p. vs. Q1’25)

- Strong Free Cash Flow LTM at €1,191 million

- Further progress in Innovation & Sustainability as New Product and Solution Vitality reaches 29.9% (28.3%, FY25), and recycled content rises to 23.3% (21.8%, FY25)

- FY26 guidance confirmed

Massimo Battaini, Prysmian CEO: “Prysmian has made impressive progress in the first quarter of the year. Continued organic growth, margin enhancement and the strong free cash flow in this quarter is the starting point for further success throughout 2026.

The geopolitical events that have opened the year have also added further impetus to the central role our solutions play in overcoming the most pressing global challenges. Prysmian unlocks energy security, accelerating the adoption of cost-effective clean generation while modernizing infrastructure through interconnectors, power grid upgrades, and enabling electrification on a global scale, including energy-hungry data centers.

Global demand for fiber and optic cables is surging, starting from data centers, creating a unique opportunity for our Digital Solutions business thanks to our in-house technology, manufacturing capacity – Prysmian is one of just a few US fiber producers - and the only player that can provide both digital and energy solutions for data centers. This strong position will be the platform for future growth, including inside data centers - a space that we haven’t exploited yet.

This first quarter, which exceeded our own expectations, underlines that we have the right strategy, determination, agility and - above all - the people we need to seize the opportunities that lie ahead of us to accelerate sustainable growth and continue creating value for all stakeholders.”

FINANCIAL HIGHLIGHTS

The Board of Directors of Prysmian S.p.A. has approved the Group’s consolidated results for the first quarter of 2026.

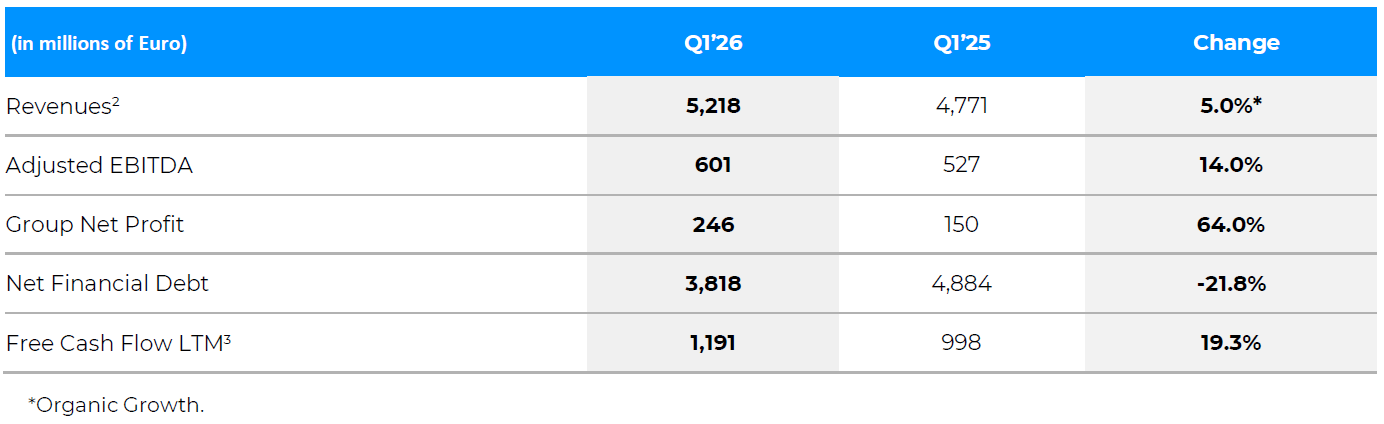

Group Revenues stood at €5,218 million in Q1’26, up from €4,771 million in Q1’25 (+5.0% organic growth).

Adjusted EBITDA stood at €601 million, up 14.0% (€527 million, Q1’25). There was an overall impact of €-36 million from foreign exchange (forex).

The overall margin at standard metal prices was 14.2%, up from 13.1% at Q1’25.

Profitability was best-in-class in Transmission, with Adjusted EBITDA of €146 million (€124 million in Q1’25) and a margin of 20.1% (16.9% in Q1’25).

Power Grid’s Adjusted EBITDA was €107 million (€116 million, Q1’25), and the margin was 12.4% versus 15.2% in Q1’25.

Industrial & Construction saw an increase in Adjusted EBITDA to €196 million (€173 million, Q1’25), and the margin increased by 1.4 p.p. versus Q1’25 to reach 13.0%.

In Specialties, Adjusted EBITDA was €64 million (€74 million, Q1’25) and the margin was substantially stable at 11.1%.

Positive momentum continued in Digital Solutions, with Adjusted EBITDA rising to €88 million (€42 million, Q1’25) and the margin growing by 7.4 p.p. versus Q1’25 to reach 20.6%.

EBITDA increased to €579 million (€507 million, Q1’25).

Net profit was €253 million (€246 million attributable to Group shareholders) versus €155 million (€150 million attributable to Group shareholders) in Q1’25.

Free Cash Flow LTM rose to €1,191 million, up from €1,171 in FY25.

Net Financial Debt decreased to €3,818 million from €4,884 million on March 31, 2025. The decrease mainly reflects:

- Free Cash Flow for €1,191 million generated by

- €2,029 million net cash flow provided by operating activities (before changes in net working capital);

- €105 million net cash flow released by changes in net working capital;

- €746 million cash outflows for net capital expenditure;

- €205 million payments of net finance costs;

- €8 million dividends received from associates;

- the issued hybrid bond (net effect decreasing net debt for €943 million);

- proceeds from the sale of the stake in YOFC and other disposals for €675 million;

- M&A activities, mainly the acquisition of Channell (+€1,206 million);

- the dividend paid to shareholders (+€248 million).

Media relations

Lauren Kane

External Communications Manager, North America

- phone+1 859.572.8825

- email[email protected]

Media relations

Anna Wright

Vice President of Marketing & Communications, North America

- phone+1 859.572.8793

- email[email protected]